Important Factors to Consider Before Buying Any Insurance

Important Factors to Consider Before Buying Any Insurance

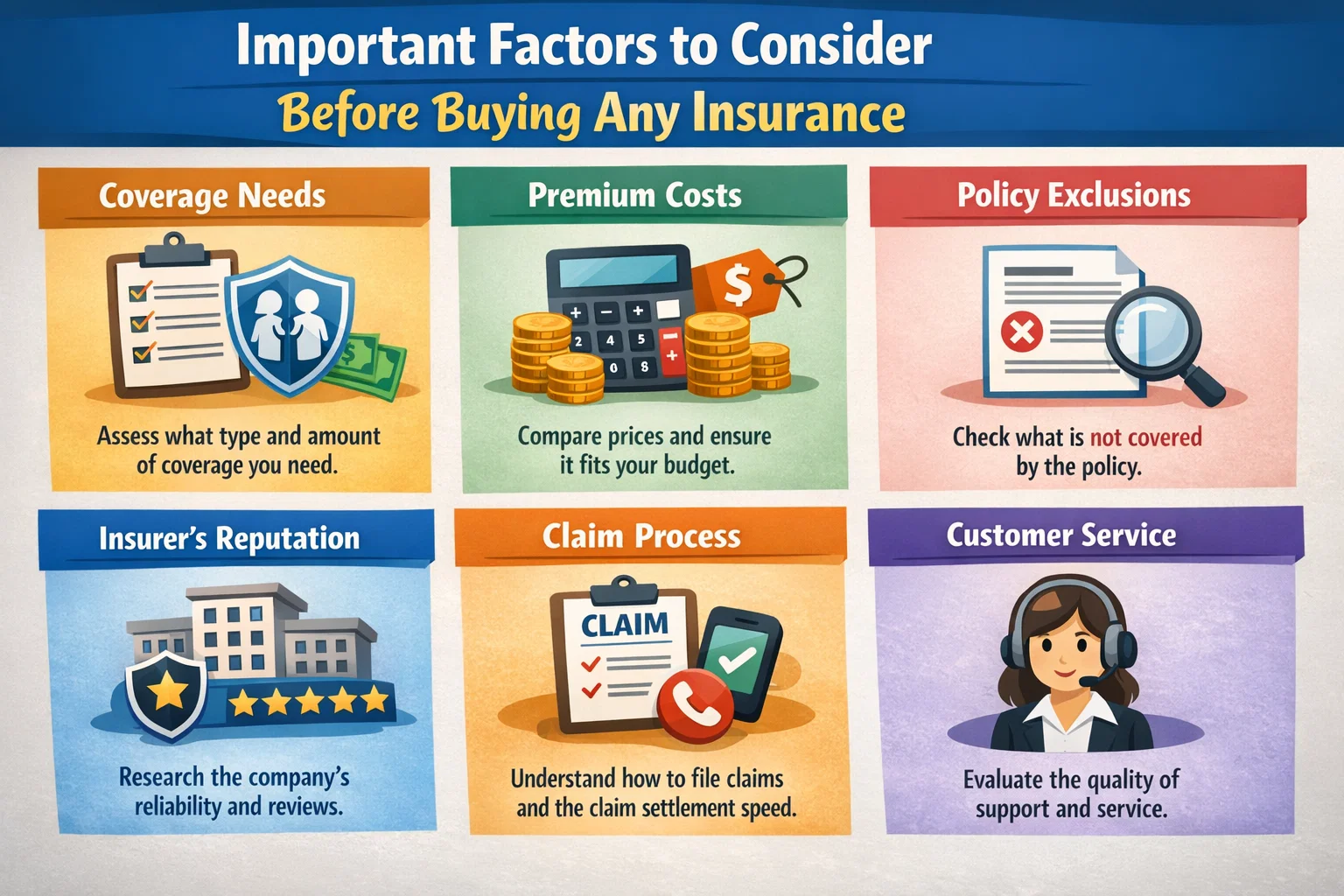

Buying insurance is not just a financial decision—it is a long-term commitment that protects you, your family, and your assets against unexpected risks. Whether you are purchasing health insurance, life insurance, car insurance, or travel insurance, understanding the important factors to consider before buying any insurance can save you from costly mistakes and future stress.

In Tier 1 countries like the United States, United Kingdom, Canada, and Australia, insurance costs are high, claim processes are strict, and exclusions can significantly impact payouts. This comprehensive guide will walk you through every critical factor you must evaluate before buying any insurance policy, helping you make a smart, professional, and future-proof decision.

Why Choosing the Right Insurance Matters

Many people buy insurance quickly—often influenced by low premiums, aggressive agents, or online ads. Unfortunately, this leads to underinsurance, claim rejections, or paying for coverage that doesn’t align with real needs.

Choosing the right insurance ensures:

- Financial protection during emergencies

- Peace of mind for you and your family

- Lower out-of-pocket expenses

- Better long-term financial planning

Factor 1: Identify Your Actual Insurance Needs

The first and most important step before buying any insurance is identifying your real needs. Different people face different risks based on age, income, lifestyle, dependents, and location.

Questions to Ask Yourself

- What risks am I trying to protect against?

- Do I have financial dependents?

- What assets need protection?

- How much coverage is enough?

Without clarity, even the best policy can turn out to be useless.

Factor 2: Type of Insurance Policy

Each type of insurance serves a different purpose. Buying the wrong type can lead to poor coverage or unnecessary expenses.

| Insurance Type | Primary Purpose |

|---|---|

| Health Insurance | Covers medical and hospitalization expenses |

| Life Insurance | Provides financial security to dependents |

| Car Insurance | Protects against vehicle damage and liability |

| Travel Insurance | Covers travel-related emergencies |

Always choose the policy type based on risk exposure, not popularity.

Factor 3: Coverage Amount (Sum Insured)

One of the most critical insurance buying factors is choosing the right coverage amount. Too little coverage leaves you vulnerable, while excessive coverage increases premiums unnecessarily.

In Tier 1 countries, medical bills, legal liabilities, and living expenses are extremely high. Always factor in inflation and future costs.

How to Decide Coverage

- Income replacement needs

- Outstanding loans

- Medical inflation

- Dependents’ future expenses

Factor 4: Premium Affordability

Premium affordability is important, but it should never be the sole deciding factor. A cheaper premium often means reduced coverage, higher deductibles, or more exclusions.

A good rule: choose a premium that fits your budget without compromising essential coverage.

Factor 5: Policy Inclusions and Benefits

Inclusions define what the insurance policy actually covers. Two policies with similar premiums can offer vastly different benefits.

Key Inclusions to Check

- Hospitalization and emergency coverage

- Worldwide or Tier 1 country coverage

- Critical illness benefits

- Accidental death or disability cover

- Cashless claim facilities

Factor 6: Exclusions and Limitations

Exclusions are conditions where claims will not be paid. Ignoring them is one of the most expensive mistakes buyers make.

Common Exclusions Across Insurance Types

- Pre-existing medical conditions

- Self-inflicted injuries

- Alcohol or substance abuse

- High-risk activities

- War or terrorism-related events

Always read exclusions carefully before buying.

Factor 7: Deductibles and Co-Payment

Deductibles and co-payments determine how much you pay from your own pocket during a claim. Lower premiums often come with higher deductibles.

Balance affordability with reasonable out-of-pocket costs.

Factor 8: Claim Settlement Ratio and Claim Process

The claim settlement ratio (CSR) reflects an insurer’s reliability. A high CSR usually means faster and smoother claim approvals.

- Check historical claim settlement data

- Read customer reviews

- Understand documentation requirements

In high-cost healthcare systems, claim reliability is crucial.

Factor 9: Insurer Reputation and Financial Stability

An insurance policy is only as good as the company backing it. Financially strong insurers are more likely to honor claims even during economic downturns.

Prefer insurers with global presence, strong credit ratings, and transparent operations.

Factor 10: Policy Term and Renewal Conditions

Always check how long the policy lasts and the renewal terms. Some policies become expensive or restrictive after renewal.

- Lifetime renewability

- Guaranteed renewal clauses

- Premium revision history

Factor 11: Riders and Add-On Benefits

Riders enhance coverage and often provide excellent value for money.

Popular High-Value Riders

- Critical illness rider

- Accidental death benefit

- Waiver of premium

- Zero depreciation (vehicle insurance)

Factor 12: Long-Term Cost vs Short-Term Savings

Insurance should be evaluated over the long term. A policy that looks cheap today may become expensive later.

Always analyze costs over 5–20 years, especially for life and health insurance.

Factor 13: Tax Benefits and Legal Compliance

In many countries, insurance premiums offer tax deductions. While tax savings should not be the primary reason to buy insurance, they do improve overall value.

Common Mistakes to Avoid Before Buying Insurance

- Buying insurance without comparing options

- Choosing based only on premium

- Ignoring exclusions and fine print

- Over-insuring or under-insuring

- Trusting agents blindly

Expert Tips for Buying the Right Insurance

- Compare at least 3–5 policies

- Match coverage with real-life risks

- Review policy annually

- Keep documentation organized

- Choose transparency over brand popularity

Final Thoughts

Understanding the important factors to consider before buying any insurance empowers you to make informed, confident, and financially sound decisions. In today’s world of rising costs and complex policies, taking the time to evaluate coverage, exclusions, insurer reliability, and long-term value is not optional—it’s essential.

The right insurance policy doesn’t just protect your money—it protects your future.

Comments (3)